Between the Fed’s aggressive policy tightening to rein in inflation and deteriorating economic data, volatility has become a seemingly ever-present facet of the stock market. While the current economic landscape has spurred fear among investors, others view market volatility as a unique buying opportunity.

Opportunity is the key word – and sometimes the hardest thing for investors to see. To find names that can deliver solid returns and now come with a bargain price tag, investors will often turn to penny stocks, or those trading for less than $5 per share.

Sure, there could be a very good reason these tickers are so affordable, but should there be even minor share price appreciation, massive percentage gains could materialize, along with hefty profits for investors.

So, how are investors supposed to determine which names have what it takes to make a comeback? Follow the pros.

Using TipRanks’ database, we were able to pinpoint two promising penny stocks, according to Wall Street analysts. Both tickers boast a Strong Buy consensus rating and could climb over 300% higher in the year ahead.

VistaGen Therapeutics (VTGN)

We’ll start with VistaGen, a biopharmaceutical research company with a focus on disorders of the central nervous system. The company’s leading programs are new treatments for anxiety and depression, serious conditions with large potential patient bases. According to recent governmental health authority data, some 264 million people worldwide suffer from depression-related disorders, 19.4 million US adults have experienced at least one major depressive episode, and some 25 million people suffer from social anxiety disorders (SADs) in the US alone. This is the population that VistaGen aims to help.

The company has three main drug candidate programs, each one with a different pharmacological mode of action and target condition. The leading candidate is PH94B, a new treatment for social anxiety disorder. The drug, administered by nasal spray, is currently undergoing the PALISADE clinical trials. PALISADE-1, a phase 3 study that followed 208 patients across 15 clinical sites in the US, is focused on the use of PH94B as an acute treatment for rapid onset anxiety in adults. VistaGen announced last month that the study is now complete, and topline results will be available this year. PALISADE-2, another phase 3 trial of identical size and scope, in still underway, with topline results expected in late 2022. PH94B has been granted ‘fast track’ status by the FDA.

The other two clinical programs, PH10 and AV-101, are less advanced. PH10 is under development as a treatment for depression, and is also administered as a nasal spray. An exploratory phase 2a trial showed promise, and VistaGen is assembling an Investigational New Drug application for the FDA, to gain approval for a phase 2b clinical trial of PH10 in the treatment of major depressive disorder.

AV-101, a drug candidate being studies as a treatment for neurological disorders, is the subject of a phase 1b drug-drug interaction study, in combination with probenecid. AV-101 is an orally dosed product, and VistaGen is considering further trials as a combination therapy with probenecid.

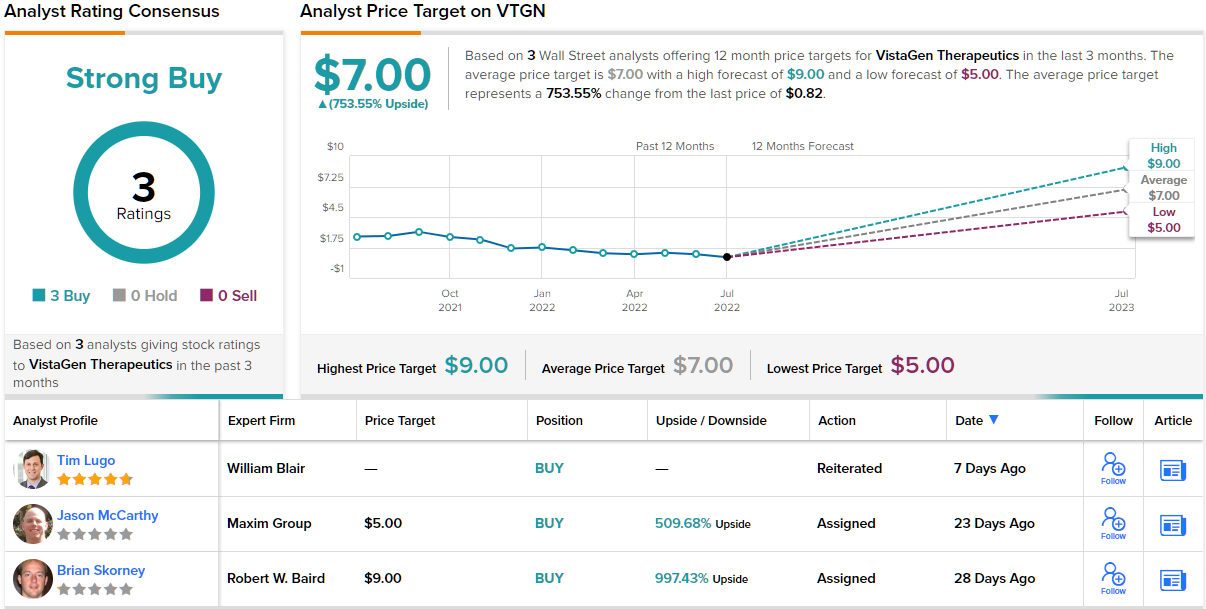

Currently going for only $0.82 apiece, at least one member of the Street believes that now is the right time to snap up shares.

Baird’s Brian Skorney has reviewed VistaGen’s current position and sees plenty to be optimistic about. The key point, in his view, is the soon-to-be-released data from PALISADE-1, which should give investors reason to buy in.

“We continue to view the inbound top-line readout, expected no later than mid-August, as a crucial catalyst for the PH94B opportunity in SAD. We continue to think the existing data support the expectation that the study will hit on its primary endpoint, offering a favorable risk/reward at the current valuation,” Skorney opined.

“We continue to see substantial upside potential with PH94B in SAD and other forms of anxiety disorders, and believe current valuation of VTGN underestimates the clinical proof of concept and the commercial potential,” the analyst added.

To this end, Skorney rates VTGN an Outperform (i.e. Buy), and his price target, at $9, suggests just how much he expects that outperformance: up to 997% in the coming year. (To watch Skorney’s track record, click here)

Other analysts are on the same page. With 2 additional Buy ratings, the word on the Street is that VTGN is a Strong Buy. On top of this, the average price target is $7, suggesting robust growth of ~754%. (See VTGN stock forecast on TipRanks)

Oyster Point Pharma (OYST)

The second stock we’ll look at is another biopharma, one in both the clinical and commercialization stages. Oyster Point is working on new treatments for ophthalmic diseases, and is focuses on first-in-class therapies, including small molecule and gene therapy approaches, to better eye health. The company currently has programs at various stages of development, from pre-clinical research to early stage human clinical trials to an FDA-approved product on the market.

The current clinical trial, of OC-01 as a treatment for neurotrophic keratopathy, is at Phase 2 in the US, with patient enrollment continuing for the OLYMPIA clinical study. Preliminary results from this study are expected in 2H22. In addition, the company has announced that it has received authorization to proceed with a Phase 3 study of OC-01 in the Chinese market.

On the commercial side, Oyster Point received its first FDA approval in October of last year. That drug, now branded as tyrvaya, is a nasal spray treatment for dry eye disease. During 1Q22, the last quarter reported, Oyster Point saw net product revenues related to tyrvaya of $2.7 million. This was driven by 19,000 prescriptions written and filled during the quarter; more than 4,500 eye care providers recommended the drug. The company has also been successful in securing insurance approvals of the medication, and commercial coverage for tyrvaya is now available for 95 million people.

It is important to note here that tyrvaya and OC-01 are the same compound, varenicline solution. The branded name applies to the drug’s approved use in dry eye disease.

H.C. Wainwright analyst Matthew Caufield believes that OYST shares are now badly underpriced, given the company’s strong start with tyrvaya. He writes, “With November 2021 launch along with February 2022 announced coverage by Express Scripts, Tyrvaya has more than doubled the reported unique prescribers from approximately 1,900 during the YE21 launch, to greater than 4,500 unique prescribers through 1Q22. We highlight these trends represent the earliest stages of Tyrvaya launch, along with anticipated coverage determinations for all major US commercial payors during mid-2022, which we believe can serve as an important catalyst for near-term commercial growth.”

The analyst continued, “We do not believe the discounted pricing for OYST is warranted, particularly based on the viability of its lead commercial asset Tyrvaya, in our view. More broadly, we believe DED patients can benefit from the differentiated nasal spray delivery and mechanism of action that specifically addresses tear film homeostasis, tolerability, and timely onset of action.”

All of that is a fair case for Caufield’s Buy rating on the shares, and his $20 price target implies a robust 303% upside for the next 12 months. (To watch Caufield’s track record, click here)

Overall, Oyster Point has picked up 3 recent analyst reviews from the Street – and they are all positive, for a unanimous Strong Buy consensus rating. OYST shares have a current trading price of $4.96 and an average price target of $24, suggesting the stock will gain ~384% in the year ahead. (See OYST stock forecast at TipRanks.)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Source: https://finance.yahoo.com/news/2-strong-buy-penny-stocks-144233815.html